Consent is considered to be free consent when the following factors are satisfied: It should be free from coercion. The contract should not be done under the pressure of undue influence. The contract should be done without fraud.

Q. What is a free consent?

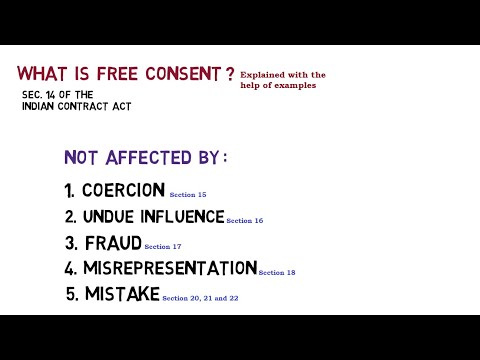

Free Consent. According to Section 13, ” two or more persons are said to be in consent when they agree upon the same thing in the same sense (Consensus-ad-idem). According to Section 14, Consent is said to be free when it is not caused by coercion or undue influence or fraud or misrepresentation or mistake.

Table of Contents

- Q. What is a free consent?

- Q. What is free consent with example?

- Q. How do you think free consent is vitiated?

- Q. What are the causes that vitiates consent?

- Q. What does rescission mean?

- Q. What is a rescission offer?

- Q. What are the effects of rescission?

- Q. What are the two types of rescission?

- Q. What is rescission of Judgement?

- Q. What is the purpose of rescission?

- Q. What are rescission rights?

- Q. Can I cancel a contract after signing?

- Q. Who signs the right of rescission?

- Q. Who should receive the rescission notice?

- Q. Do all refinances contain the Notice of Right to Cancel?

- Q. Can Lender cancel loan after closing?

- Q. When would the right of rescission period end?

- Q. What is rescission date?

- Q. Can you back out of mortgage before closing?

- Q. Can you walk away from a refinance?

- Q. What happens if you back out before closing?

- Q. Can I back out of an intent to proceed?

Q. What is free consent with example?

In the Indian Contract Act, the definition of Consent is given in Section 13, which states that “it is when two or more persons agree upon the same thing and in the same sense”. So the two people must agree to something in the same sense as well. Let’s say for example A agrees to sell his car to B.

Q. How do you think free consent is vitiated?

A contract is voidable if it is made in the absence of a free will. So, in order to constitute a free consent, it should be kept in mind that the consent is not backed by coercion, undue influence, fraud, misrepresentation or mistake.

Q. What are the causes that vitiates consent?

The main vitiating factors in the law of contract are: misrepresentation, mistake, undue influence, duress, incapacity, illegality, frustration and unconscionability. A misrepresentation is an untrue or misleading statement of fact which induces a person into a contract.

Q. What does rescission mean?

rendered null and void

Q. What is a rescission offer?

A: A rescission offer is an offer by the issuer of securities to repurchase those securities and refund their purchase price plus interest.

Q. What are the effects of rescission?

Dragon:34 Rescission has the effect of “unmaking a contract, or its undoing from the beginning, and not merely its termination.” Hence, rescission creates the obligation to return the object of the contract. It can be carried out only when the one who demands rescission can return whatever he may be obliged to restore.

Q. What are the two types of rescission?

There are two kinds of rescission, namely rescission in equity and rescission de futuro. Also referred to as rescission ab initio, i.e., from the beginning, rescission in equity works by rolling back the contract to the initial state of affairs, before the parties in question accepted the terms of the contract.

Q. What is rescission of Judgement?

Essentially, a default judgment is attached to your name when a Court makes a finding that you are liable for a debt, either if you do not defend the claim or during a case if you fail to act in accordance with the Court Rules. …

Q. What is the purpose of rescission?

The purpose of rescission is to restore the status quo ante, ie the state of affairs existing before the contract was entered into. When a contract transferring title to property is rescinded, it usually has the effect of re-vesting any property so transferred in the transferor.

Q. What are rescission rights?

The right of rescission is the right of a borrower to cancel a home equity loan, line of credit or refinancing agreement within a 3-day period without financial penalty. It was born out of the Truth in Lending Act (TILA).

Q. Can I cancel a contract after signing?

There is a federal law (and similar laws in every state) allowing consumers to cancel contracts made with a door-to-door salesperson within three days of signing. The three-day period is called a “cooling off” period.

Q. Who signs the right of rescission?

Established by the Truth in Lending Act (TILA) under U.S. federal law, the right of rescission allows a borrower to cancel a home equity loan, line of credit, or refinance with a new lender, other than with the current mortgagee, within three days of closing.

Q. Who should receive the rescission notice?

Who receives notice. Each consumer entitled to rescind must be given two copies of the rescission notice and the material disclosures. In a transaction involving joint owners, both of whom are entitled to rescind, both must receive the notice of the right to rescind and disclosures.

Q. Do all refinances contain the Notice of Right to Cancel?

If you are buying a home with a mortgage, you do not have a right to cancel the loan once the closing documents are signed. If you are refinancing a mortgage, you have until midnight of the third business day after the transaction to rescind (cancel) the mortgage contract.

Q. Can Lender cancel loan after closing?

The lender has no right of rescission. Once you have signed loan documents, you have entered into a binding contract, and the lender is legally bound to honor those signed documents. The right of rescission is a separate form giving you three days in which you can back out of the transaction without penalty.

Q. When would the right of rescission period end?

When the Right of Rescission Period Begins and Ends The rescission period begins at midnight the day after loan documents are signed, and ends three business days later, including Saturdays, but not Sundays or federal holidays.

Q. What is rescission date?

The rescission date is three business days after the signing date, the date the borrower receives the Truth in Lending Disclosure, or the date the borrower receives the “Notice of Right to Cancel”, whichever occurs last. Some lenders may use varying dates when calculating their rescission, so if in doubt, call them.

Q. Can you back out of mortgage before closing?

You can back out of a mortgage before closing The seller may decide to back out of the deal, or you may have the bad luck of applying for a mortgage when interest rates are on the rise and you cannot afford a higher rate.

Q. Can you walk away from a refinance?

Real estate settlement laws protect homeowners and their equity in a refinance. You can back out of a home refinance, within a certain grace period, for any reason, but you may face a fees or penalty if you choose to cancel or otherwise can’t refinance.

Q. What happens if you back out before closing?

If you’re backing out of an offer without a contingency, you risk losing your earnest money. Since you put that money down based on the promise you’ll follow through with the contract, backing out for any reason that’s not outlined in the agreement means the seller is legally permitted to keep your money.

Q. Can I back out of an intent to proceed?

The intent to proceed simply authorizes the lender to start working on your file. You are free to examine opportunities until your loan funds. Sure you can, as Amber said above you can back out right up until everything is completed. You are not obligated to complete the loan process.